http://www.gannglobal.com/webinar/2016/August/321gold/16-08-Video1.php

Can you say 20008?

Wednesday, August 31, 2016

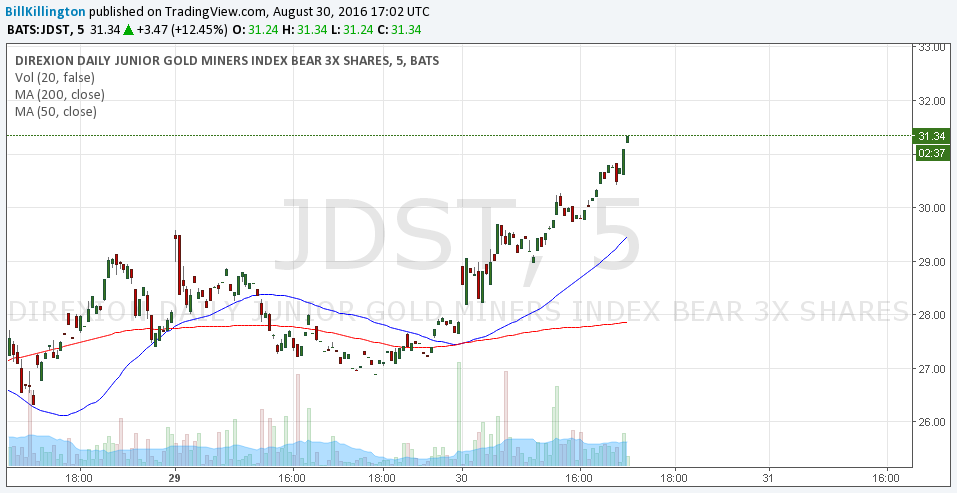

JDST ( possible tripple top in play? )

Went long NUGT at these prices its a no brainier, way to much bearishness and the DXY is not confirming this move.

Note I am still holding JDST one more day or maybe as long as Friday after NFP just to be safe let's see if they a pull a final blood bath phase to hit the lower stops.

This is just the bankers buying cheap shares for the next cycle leg..again ...the DXY is not confirming this bearishness fact is it stalled today and failed the 50ma once again ... Telling

Bill Gross on CNBC

- Yes, the Fed will raise rates in September

- Pension funds must lower expectations on payments

- Removing Rousseff doesn't improve Brazilian bonds

- The Fed believes low rates are a positive; I think they're negative

- We need classic fiscal stimulus

- The central bank basically says to the fiscal authority that you don't need to pay

- "Let's raise rates in Sept and again in 6-9 months"

- There are 11 trillion in negative rate bonds; those are liabilities, not assets

Abercrombie & Fitch closing up to 60 stores nationally

http://www.wrcbtv.com/story/32899948/abercrombie-fitch-closing-up-to-60-stores-nationally

Abercrombie & Fitch Co. reported a wider loss for its second quarter on Tuesday and said it's closing up to 60 stores in the United States as both U.S. and international sales fell.

The teen-focused retailer also offered a downbeat outlook for a key sales measure, as business continues to be hurt by a decline in tourists to its flagships in key cities. The closures will represent about 8 percent of its store count in the domestic market. Abercrombie's shares tumbled more than 20 percent in midday trading.

Abercrombie, once a top destination for teens, has struggled to adjust as its customers increasingly shop on their phones and other mobile devices, and shift more to fast-fashion chains like H&M. The retailer is changing its marketing to play down its sexy image, and last year got rid of provocative pictures on its shopping bags and bare-chested male models greeting customers at the door. It also gave employees more freedom to dress how they wish, ditching its "look policy" that banned eyeliner and certain hairstyles among other rules.

Abercrombie & Fitch Co. reported a wider loss for its second quarter on Tuesday and said it's closing up to 60 stores in the United States as both U.S. and international sales fell.

The teen-focused retailer also offered a downbeat outlook for a key sales measure, as business continues to be hurt by a decline in tourists to its flagships in key cities. The closures will represent about 8 percent of its store count in the domestic market. Abercrombie's shares tumbled more than 20 percent in midday trading.

Abercrombie, once a top destination for teens, has struggled to adjust as its customers increasingly shop on their phones and other mobile devices, and shift more to fast-fashion chains like H&M. The retailer is changing its marketing to play down its sexy image, and last year got rid of provocative pictures on its shopping bags and bare-chested male models greeting customers at the door. It also gave employees more freedom to dress how they wish, ditching its "look policy" that banned eyeliner and certain hairstyles among other rules.

China's Biggest-Ever Metals Deal Snaps Up Cleveland's Aleris

http://www.bloomberg.com/news/articles/2016-08-30/china-s-biggest-ever-metals-deal-snaps-up-cleveland-s-aleris

China's influence in global metals markets just stepped up a gear after the owner of its top supplier of aluminum products agreed to buy Aleris Corp. of the U.S. for $2.3 billion, marking the nation's biggest-ever overseas purchase of a metals processor.

...

China Zhongwang is Asia's biggest producer of extruded aluminum, and already has ambitions to sell aluminum sheet to China's emerging auto and aerospace industries. It's due this year to start up a flat-rolled aluminum plant in Tianjin, near Beijing, which will supply products that China still has to import.

China's influence in global metals markets just stepped up a gear after the owner of its top supplier of aluminum products agreed to buy Aleris Corp. of the U.S. for $2.3 billion, marking the nation's biggest-ever overseas purchase of a metals processor.

...

China Zhongwang is Asia's biggest producer of extruded aluminum, and already has ambitions to sell aluminum sheet to China's emerging auto and aerospace industries. It's due this year to start up a flat-rolled aluminum plant in Tianjin, near Beijing, which will supply products that China still has to import.

Meet TISA, the 'secret privatisation pact that poses a threat to democracy'

http://www.independent.co.uk/news/business/news/ttip-trade-deal-new-what-is-tisa-privatisation-pact-secret-threat-to-democracy-a7216296.html

Few people may have heard of the Trade In Services Agreement, but campaign group Global Justice Now warns in a new report: "Defeating TTIP may amount to a pyrrhic victory if we allow TISA to pass without challenge."

Like the Transatlantic Trade and Investment Partnership, TISA is being negotiated in secret, even though it could have a major impact on countries which sign up.

...

"TISA threatens public services. From postal services to the NHS, TISA could lock in privatisation and ensure that big multinationals increasingly call the shots on areas like health, education and basic utilities."

A so-called "ratchet" clause in the deal means that after a service -- like trains or water or energy -- is privatised, this is almost impossible to reverse even if it fails.

Few people may have heard of the Trade In Services Agreement, but campaign group Global Justice Now warns in a new report: "Defeating TTIP may amount to a pyrrhic victory if we allow TISA to pass without challenge."

Like the Transatlantic Trade and Investment Partnership, TISA is being negotiated in secret, even though it could have a major impact on countries which sign up.

...

"TISA threatens public services. From postal services to the NHS, TISA could lock in privatisation and ensure that big multinationals increasingly call the shots on areas like health, education and basic utilities."

A so-called "ratchet" clause in the deal means that after a service -- like trains or water or energy -- is privatised, this is almost impossible to reverse even if it fails.

U.S. Treasuries are Heading for Their Biggest Monthly Loss Since June 2015

Treasury securities traders are beginning to fear a Federal Reserve rate hike later this year.

There is no chance the Fed is going to reverse the December 2015 rate hike anytime soon. Holding the view that a near-term plunge to negative rates in the U.S. is likely is the height of confusion about the current state of the economy and how the Federal Reserve operates.

Nigeria Price Inflation Accelerates to Highest in Nearly 11 Years

When you can't sell oil that you pump for top dollar, I guess the solution is to just print money.

Nigerian inflation accelerated for the ninth consecutive month in July.

The inflation rate increased to 17.1 percent from 16.5 percent in June, the Abuja-based National Bureau of Statistics said in a statement issued today.

Global central bankers, stuck at zero, unite in plea for help from governments

https://ca.news.yahoo.com/global-central-bankers-stuck-zero-unite-plea-help-123135496--business.html

Central bankers in charge of the vast bulk of the world's economy delved deep into the weeds of money markets and interest rates over a three-day conference here, and emerged with a common plea to their colleagues in the rest of government: please help.

Central bankers in charge of the vast bulk of the world's economy delved deep into the weeds of money markets and interest rates over a three-day conference here, and emerged with a common plea to their colleagues in the rest of government: please help.

Mired

in a world of low growth, low inflation and low interest rates,

officials from the Federal Reserve, Bank of Japan and the European

Central Bank said their efforts to bolster the economy through monetary

policy may falter unless elected leaders stepped forward with bold

measures. These would range from immigration reform in Japan to

structural changes to boost productivity and growth in the U.S. and

Europe.

US EIA weekly oil inventories +2276K vs +1300K expected

- Prior was +2501K

- Gasoline -691K vs -1000K exp

- Distillates +1496K vs -125K exp

- Cusing inventory -1039K vs +400K

- Production -0.7% w/w and -7.9% y/y

Expect Big Gold and Silver RAID Tomorrow! – Harvey Organ

http://www.silverdoctors.com/silver/silver-news/expect-big-gold-and-silver-raid-tomorrow-harvey-organ/

He nailed it...

EXPECT A GOOD SIZED RAID ON GOLD AND SILVER AHEAD OF TOMORROW’S OTC/LBMA EXPIRY…

BOTH RUSSIA AND THE USA ANGRY AT TURKEY’S INVASION OF SYRIA/AFTER TODAY’S GRAB BY THE EU ON APPLE, THEY SET THEIR SIGHTS ON AMAZON AND MCDONALD’S/ THE FBI UNCOVER EMAILS FROM HILLARY’ SERVER ON BENGHAZI AND THUS SHE LIED UNDER OATH/GOOD SIZED RAID ON GOLD AND SILVER AHEAD OF TOMORROW’S OTC/LBMA EXPIRY

He nailed it...

EXPECT A GOOD SIZED RAID ON GOLD AND SILVER AHEAD OF TOMORROW’S OTC/LBMA EXPIRY…

BOTH RUSSIA AND THE USA ANGRY AT TURKEY’S INVASION OF SYRIA/AFTER TODAY’S GRAB BY THE EU ON APPLE, THEY SET THEIR SIGHTS ON AMAZON AND MCDONALD’S/ THE FBI UNCOVER EMAILS FROM HILLARY’ SERVER ON BENGHAZI AND THUS SHE LIED UNDER OATH/GOOD SIZED RAID ON GOLD AND SILVER AHEAD OF TOMORROW’S OTC/LBMA EXPIRY

Friday’s Jobs Report Could Trigger A Stock Market CRASH – Stewart Thomson

http://www.silverdoctors.com/gold/gold-news/fridays-jobs-report-could-trigger-a-stock-market-crash-stewart-thomson/

- At the current pace of quantitative easing, Japan’s central bank is buying so many bonds that it now has about 24 months left before there are no more bonds left to buy.

- The BOJ is buying close to $800 billion (USD) of bonds annually. The bank’s QE program is truly gargantuan, and Kuroda made a key speech at Jackson Hole indicating he has no intention of tapering it at all.

- Please click here now. Gold is extremely well-supported now, by both equity fund and FOREX money managers.

- Kuroda hinted at Jackson Hole that while he won’t taper QE, he has substantial room to increase the use of his negative rates program. He’s making another key speech next Monday, and I expect him to make it clear that as enormous as his QE program is, he’s going to lower interest rates further, and make it even more important policy than QE.

- The US jobs report is scheduled for release this Friday at 8:30AM. When Janet Yellen hiked rates last December, a huge institutional panic out of stock markets and the dollar developed.

- These institutions surged into gold and the yen. A big jobs report number is likely to spur Janet to unveil a second rate hike at the September 21 FOMC meeting.

- This is probably the most important jobs report of the entire year, and Janet’s reaction to it could begin a major stock market and US dollar crash.

- The September and October time-frame is what I call “US stock market crash season”. The worst stock market crashes have historically occurred during these months, and Friday’s jobs report has the potential to create another one.

- Gold price enthusiasts should pay keen attention to all the upcoming speeches made by key players at both the BOJ and the Fed. Those speeches and policy decisions are likely to create important changes on the charts that gold market technicians focus on.

Chicago PMI 51.5 vs 54.0 expected

- Prior was 55.8

- Inventories 49.8 vs 52.0 prior

- Employment highest since April 2015

- New orders and production at lowest since May

- Prices paid lowest since March

US July pending home sales +1.3% vs +0.7% m/m expected

- Prior was +0.2% m/m (revised to -0.8%)

- Sales -2.2% y/y vs +2.2% exp

- Prior y/y reading was +0.3% (revised to -0.7%)

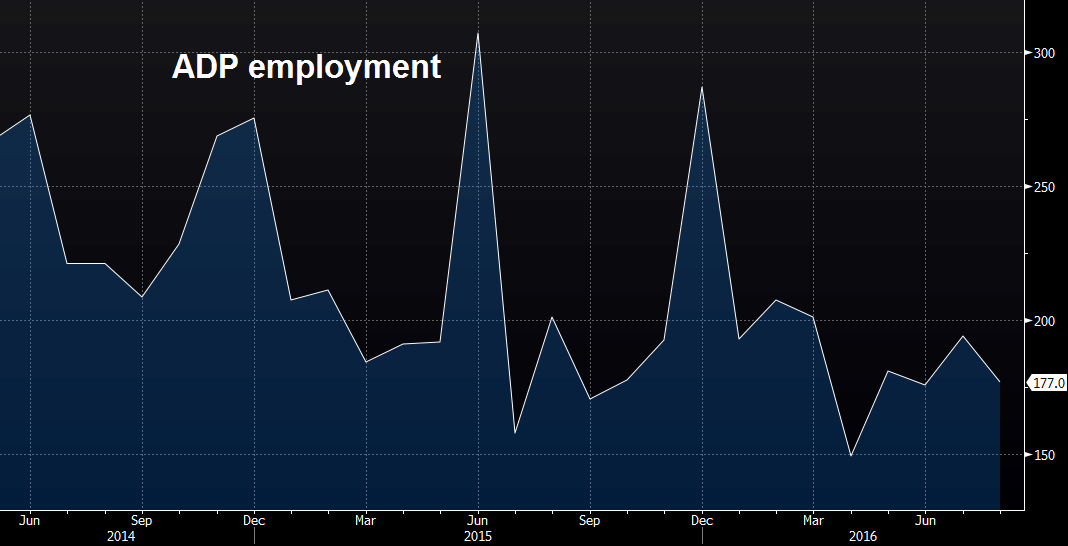

ADP August employment +177K vs +175K expected

- Prior was 179K (revised to 194K)

- Economist estimates ranged from 225K to 135K

On its own, I don't know if the Fed will take anything away from this. Over the past five months, the average ADP employment gain is 175K, which is the lowest since July 2013.

SWIFT discloses more cyber thefts, pressures banks on security

http://uk.reuters.com/article/us-cyber-heist-swift-idUKKCN11600C

SWIFT, the global financial messaging system, on Tuesday disclosed new hacking attacks on its member banks as it pressured them to comply with security procedures instituted after February's high-profile $81 million heist at Bangladesh Bank.

In a private letter to clients, SWIFT said that new cyber-theft attempts - some of them successful - have surfaced since June, when it last updated customers on a string of attacks discovered after the attack on the Bangladesh central bank.

"Customers’ environments have been compromised, and subsequent attempts (were) made to send fraudulent payment instructions," according to a copy of the letter reviewed by Reuters. "The threat is persistent, adaptive and sophisticated - and it is here to stay."

So they're basically admitting we want to monitor all transactions

SWIFT, the global financial messaging system, on Tuesday disclosed new hacking attacks on its member banks as it pressured them to comply with security procedures instituted after February's high-profile $81 million heist at Bangladesh Bank.

In a private letter to clients, SWIFT said that new cyber-theft attempts - some of them successful - have surfaced since June, when it last updated customers on a string of attacks discovered after the attack on the Bangladesh central bank.

"Customers’ environments have been compromised, and subsequent attempts (were) made to send fraudulent payment instructions," according to a copy of the letter reviewed by Reuters. "The threat is persistent, adaptive and sophisticated - and it is here to stay."

So they're basically admitting we want to monitor all transactions

US MBA mortgage applications w-e 26 Aug 2.8% vs -21.% prev

- 30-year mortgage rate 3.67% as prev

- mortgage refinance index 2441.7 vs 2355.2 prev

- purchase index 216.1 vs 213.4 prev

- mortgage market index 545.2 vs 530.1 prev

Not a price mover in its own right but all to throw into the mix

Milton Friedman and Phil Donahue On Socialism v. Capitalism

Very few people in history are as dank as Milton Friedman. Trump’s

policies are heavily informed by him – even trade, if you study the

complexities of the issue. Trump always says he isn’t against free trade

– only stupid 50,000 page trade deals. Those deals don’t sound so free

to me.

policies are heavily informed by him – even trade, if you study the

complexities of the issue. Trump always says he isn’t against free trade

– only stupid 50,000 page trade deals. Those deals don’t sound so free

to me.

Wednesday

MBA Mortgage Applications

![[Report]](http://b-us.econoday.com/images/b-global/byreport_butt_new.gif)

7:00 AM ET

7:00 AM ET

7:00 AM ETNeel Kashkari Speaks8:00 AM ET

ADP Employment Report

![[Report]](http://b-us.econoday.com/images/b-global/byconsensus_butt.gif)

![[djStar]](http://b-us.econoday.com/images/b-global/djstar.gif) 8:15 AM ET

8:15 AM ET

8:15 AM ET

Chicago PMI

9:45 AM ET

9:45 AM ET

Pending Home Sales Index

10:00 AM ET

10:00 AM ET

EIA Petroleum Status Report

![[Star]](http://b-us.econoday.com/images/b-global/star.gif) 10:30 AM ET

10:30 AM ET

10:30 AM ET

Farm Prices

3:00 PM ET

3:00 PM ETCharles Evans Speaks3:15 PM ET

A Candidate’s Death Could Delay or Eliminate the Presidential Election

http://www.usnews.com/news/articles/2016-08-30/candidate-death-could-delay-or-eliminate-presidential-election

Chaos would ensue if a vacancy emerges near Election Day.

The presidential election could be delayed or scrapped altogether if conspiracy theories become predictive and a candidate dies or drops out before Nov. 8. The perhaps equally startling alternative, if there’s enough time: Small groups of people hand-picking a replacement pursuant to obscure party rules.

The scenarios have been seriously considered by few outside of the legal community and likely are too morbid for polite discussion in politically mixed company. But prominent law professors have pondered the effects and possible ways to address a late-date vacancy.

“There’s nothing in the Constitution which requires a popular election for the electors serving in the Electoral College,” says John Nagle, a law professor at the University of Notre Dame, meaning the body that officially elects presidents could convene without the general public voting.

“It’s up to each state legislature to decide how they want to choose the state’s electors,” Nagle says. “It may be a situation in which the fact that we have an Electoral College, rather than direct voting for presidential candidates, may prove to be helpful.”

Chaos would ensue if a vacancy emerges near Election Day.

The presidential election could be delayed or scrapped altogether if conspiracy theories become predictive and a candidate dies or drops out before Nov. 8. The perhaps equally startling alternative, if there’s enough time: Small groups of people hand-picking a replacement pursuant to obscure party rules.

The scenarios have been seriously considered by few outside of the legal community and likely are too morbid for polite discussion in politically mixed company. But prominent law professors have pondered the effects and possible ways to address a late-date vacancy.

“There’s nothing in the Constitution which requires a popular election for the electors serving in the Electoral College,” says John Nagle, a law professor at the University of Notre Dame, meaning the body that officially elects presidents could convene without the general public voting.

“It’s up to each state legislature to decide how they want to choose the state’s electors,” Nagle says. “It may be a situation in which the fact that we have an Electoral College, rather than direct voting for presidential candidates, may prove to be helpful.”

Fed's Fischer: Negative Rates Just Dandy

http://www.bloomberg.com/news/articles/2016-08-30/fed-s-fischer-says-negative-rates-seem-to-work-in-today-s-world

Federal Reserve Vice Chairman Stanley Fischer said negative interest rates seem to be working in other countries, while reinforcing that they aren't on the table in the U.S.

While the Fed isn't "planning to do anything in that direction," the central banks using them "basically think they're quite successful," Fischer said Tuesday on Bloomberg Television with Tom Keene in Washington. He reiterated that Fed rate increases will be data dependent without giving a specific timeline.

As we recall, Japan's Kuroda was swearing that negative rates were "off the table" until the day before they were announced...

Federal Reserve Vice Chairman Stanley Fischer said negative interest rates seem to be working in other countries, while reinforcing that they aren't on the table in the U.S.

While the Fed isn't "planning to do anything in that direction," the central banks using them "basically think they're quite successful," Fischer said Tuesday on Bloomberg Television with Tom Keene in Washington. He reiterated that Fed rate increases will be data dependent without giving a specific timeline.

As we recall, Japan's Kuroda was swearing that negative rates were "off the table" until the day before they were announced...

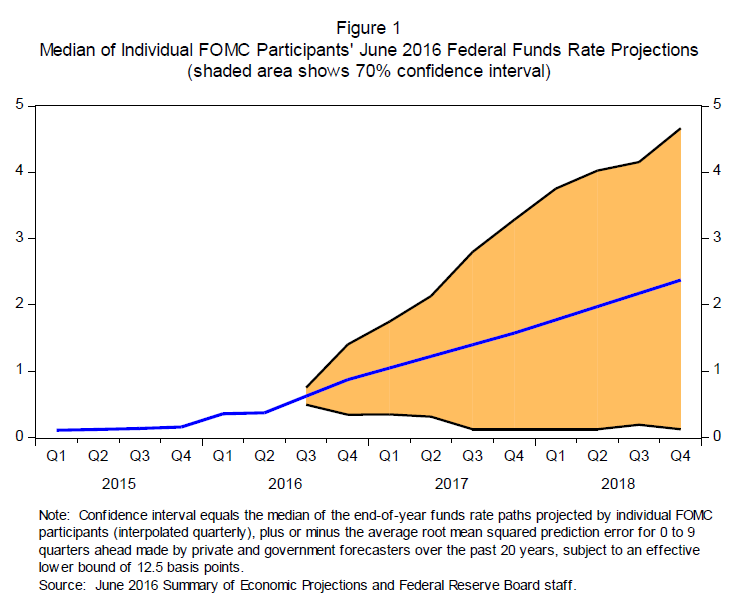

The 11 Bone-Chilling Things I Gleaned from Yellen's Chart

http://wolfstreet.com/2016/08/27/yellens-fan-chart-federal-funds-rate-projections/

hey have no clue, but they know how to talk. The chart confirms the Fed's message: They say whatever they want to in order to inflate financial markets and drive even conservative investors into huge risks without much compensation, and that's pretty much all they'll ever do.''

hey have no clue, but they know how to talk. The chart confirms the Fed's message: They say whatever they want to in order to inflate financial markets and drive even conservative investors into huge risks without much compensation, and that's pretty much all they'll ever do.''

Tuesday, August 30, 2016

If You Accept this Raise, You Fall Off the Welfare Cliff

https://fee.org/articles/if-you-accept-this-raise-you-fall-off-the-welfare-cliff/

At your present $12 an hour you are eligible for refundable tax credits, food assistance, housing assistance, child care assistance, and medical assistance worth $41,465 combined. Together with your earned income after taxes of $22,121, you are now bringing home to your kids about $63,586 a year.

If you take your employer’s offer, you’ll earn $5,451 more after taxes, $27,572. You will also become eligible for an Affordable Care Act (ACA) premium tax credit. But at that level of earned income all your other benefits would decrease by $8,336, more than your increase in net pay. That means the income you would bring home would decrease from $63,586 to $60,701.

Now you see the inner workings on how the Government traps people into the system ...

Eliminate government welfare replacing it with private charity - AS IT WAS FOR MOST OF THIS COUNTRY'S EXISTENCE.

JDST

We said to hedge I hope you did

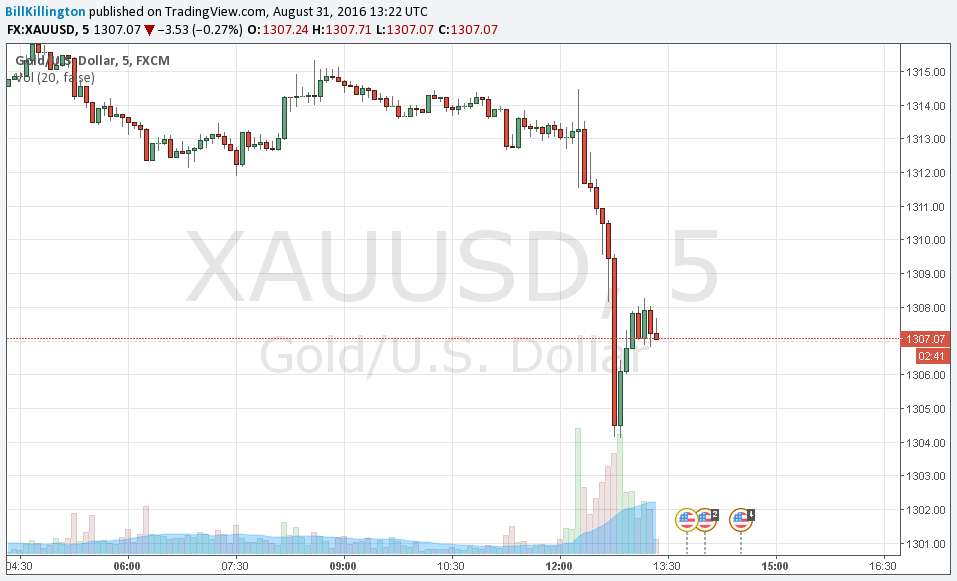

Gold @ 1312 will be an interesting moment, let see what happens.

Gold @ 1312 will be an interesting moment, let see what happens.

Europe hits Apple w $14.6B Tax Bill

http://money.cnn.com/2016/08/30/technology/apple-tax-eu-us-ireland/index.html

The tax ruling is the biggest the European Union has ever made regarding a single company, and it could spark a huge transatlantic row over how Europe treats U.S. companies.

Apple shares initially fell almost 3%, but then recovered most of their

losses. The company will appeal the decision. It said the ruling

upended the international tax system and would damage jobs and

investment in Europe.

The European Commission, which administers EU law, said the Irish government had granted illegal state aid to Apple (AAPL, Tech30) by helping the tech giant to artificially lower its tax bill for more than 20 years.

The tax ruling is the biggest the European Union has ever made regarding a single company, and it could spark a huge transatlantic row over how Europe treats U.S. companies.

The European Commission, which administers EU law, said the Irish government had granted illegal state aid to Apple (AAPL, Tech30) by helping the tech giant to artificially lower its tax bill for more than 20 years.

US Aug consumer confidence 101.1 vs 97.0 expected

- Prior was 97.3

- Highest since Sept 2015

- Present situation 123.0 vs 96.7 prior

- Expectations 86.4 vs 82.0 prior

- Jobs hard to get 23.4 vs 22.1 prior

- 1-year inflation expectations 4.8% vs 4.7% prior

The Cancer Industry is Too Prosperous to Allow a Cure

http://healthimpactnews.com/2014/the-cancer-industry-is-too-prosperous-to-allow-a-cure/

We have lost the war on cancer. At the beginning of the last century, one person in twenty would get cancer. In the 1940s it was one out of every sixteen people. In the 1970s it was one person out of ten. Today one person out of three gets cancer in the course of their life.

The cancer industry is probably the most prosperous business in the United States. In 2014, there will be an estimated 1,665,540 new cancer cases diagnosed and 585,720 cancer deaths in the US. $6 billion of tax-payer funds are cycled through various federal agencies for cancer research, such as the National Cancer Institute (NCI). The NCI states that the medical costs of cancer care are $125 billion, with a projected 39 percent increase to $173 billion by 2020.

The simple fact is that the cancer industry employs too many people and produces too much income to allow a cure to be found. All of the current research on cancer drugs is based on the premise that the cancer market will grow, not shrink.

John Thomas explains to us why the current cancer industry prospers while treating cancer, but cannot afford to cure it.

We have lost the war on cancer. At the beginning of the last century, one person in twenty would get cancer. In the 1940s it was one out of every sixteen people. In the 1970s it was one person out of ten. Today one person out of three gets cancer in the course of their life.

The cancer industry is probably the most prosperous business in the United States. In 2014, there will be an estimated 1,665,540 new cancer cases diagnosed and 585,720 cancer deaths in the US. $6 billion of tax-payer funds are cycled through various federal agencies for cancer research, such as the National Cancer Institute (NCI). The NCI states that the medical costs of cancer care are $125 billion, with a projected 39 percent increase to $173 billion by 2020.

The simple fact is that the cancer industry employs too many people and produces too much income to allow a cure to be found. All of the current research on cancer drugs is based on the premise that the cancer market will grow, not shrink.

John Thomas explains to us why the current cancer industry prospers while treating cancer, but cannot afford to cure it.

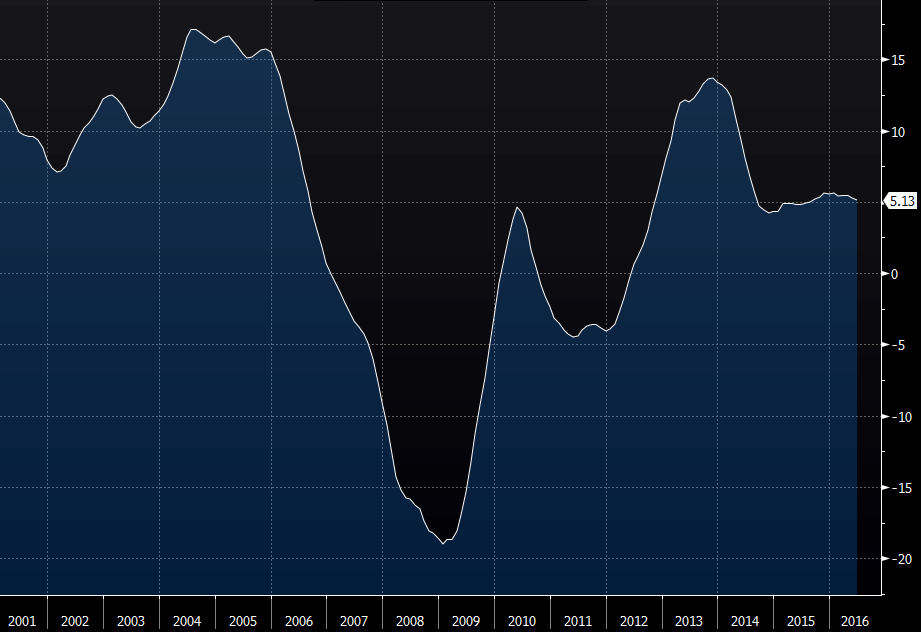

Case-Shiller June 20-city US house price index -0.07% m/m vs -0.10% exp

- Prices up 5.13% y/y vs +5.12% exp

- May prices were up 5.25% y/y

- Overall house price index +0.21% m/m vs +0.13% prior

Here's a look at the Case-Shiller house price index:

Iran has reached pre-sanctions oil output - Minister

Iran has long said it wouldn't consider a production freeze until it had regained its pre-sanctions output level.

At a conference in Norway, Deputy minister for industry, mining and trade Moazami said the country is currently producing 3.8 million barrels per day. That's up from 3.6mbpd in the latest OPEC data.

Iran's production hasn't been above 4mbpd since the 1970s.

At a conference in Norway, Deputy minister for industry, mining and trade Moazami said the country is currently producing 3.8 million barrels per day. That's up from 3.6mbpd in the latest OPEC data.

Iran's production hasn't been above 4mbpd since the 1970s.

Clinton Economist Trusts Government Too Much

https://www.bloomberg.com/view/articles/2016-08-29/heather-boushey-clinton-economist-trusts-government-too-much

From the Cowen essay:

From the Cowen essay:

This is a thoughtful and intelligent book, but for my taste Boushey holds too much faith in mandated and centralized solutions.At a blog post, though, Cowen does seem to note an important positive:

---

Boushey doesn’t estimate or indicate the expense of her proposed mandatory benefits, although she does suggest on page 1 that the cost would be “very small.” She is developing a new kind of supply-side economics, this time on the left, but like her right-wing counterparts she is running the risk of excess optimism about how much her suggested improvements will boost productivity in the system.

---

The most plausible response to these criticisms is that individual Americans cannot be trusted to make good decisions for themselves, and I am afraid that is the view being swept under the carpet here.

She is also the chief economist for Hillary Clinton’s transition team, and I would trust her with nuclear weapons.

The European Union is Collapsing

http://www.bloomberg.com/news/articles/2016-08-29/merkel-s-foreign-minister-says-post-brexit-eu-can-t-force-unity?utm_content=business&utm_campaign=socialflow-organic&utm_source=twitter&utm_medium=social&cmpid%3D=socialflow-twitter-business

“We want a ‘flexible union’ that takes on the big questions effectively, but doesn’t oblige each member state to take each new step jointly,” Steinmeier said in remarks prepared for a conference in Berlin on Monday. At the same time, EU countries that want to take joint initiatives shouldn’t be held back by those that don’t want to join in, he said.

“We want a ‘flexible union’ that takes on the big questions effectively, but doesn’t oblige each member state to take each new step jointly,” Steinmeier said in remarks prepared for a conference in Berlin on Monday. At the same time, EU countries that want to take joint initiatives shouldn’t be held back by those that don’t want to join in, he said.

Surprise: Gun Ownership Rises to 44% of All Homes

http://www.washingtonexaminer.com/surprise-gun-ownership-rises-to-44-of-all-homes/article/2600319

After a steady decline in gun ownership in recent years, more homes are reporting having a weapon inside, according to a new survey. Pew Research Center, in a poll on guns released Friday, showed that 44 percent of the country has a gun in the house. Some 51 percent don’t.

The survey firm didn’t break those numbers out for special attention in reviewing American attitudes about background checks, an assault weapon ban or other gun issues, but it shows a jump in ownership from the mid-30 percent found in other recent polls.

After a steady decline in gun ownership in recent years, more homes are reporting having a weapon inside, according to a new survey. Pew Research Center, in a poll on guns released Friday, showed that 44 percent of the country has a gun in the house. Some 51 percent don’t.

The survey firm didn’t break those numbers out for special attention in reviewing American attitudes about background checks, an assault weapon ban or other gun issues, but it shows a jump in ownership from the mid-30 percent found in other recent polls.

50 plus years of democratic rule…This is the end result! August most violent month in Chicago — in more than 20 years! Baltimore hits 200 homicides with man’s fatal stabbing

http://www.chicagotribune.com/news/local/breaking/ct-august-most-violent-shootings-chicago-20160829-story.html

Baltimore officially has had 200 homicide victims in 2016 after an autopsy confirmed a 42-year-old man found dead Friday just west of downtown had been fatally stabbed.

The victim, identified Monday as Franswhaun Smith, was found Friday about 7:50 a.m. in the 700 block of Murphy Lane, in the Heritage Crossing neighborhood that was formerly the site of the Murphy Homes public housing development.

Smith was pronounced dead at the scene. Police said an autopsy confirmed he had been stabbed in the back.

It is the fifth consecutive year Baltimore’s homicide tally has reached 200 after recording 197 in all of 2011. That was the first time the city had recorded fewer than 200 victims since the late 1970s.

Last year, 344 people were killed in Baltimore, the city’s highest highest-per capita rate ever.

As of Aug. 20, the most recent data available, homicides were down 11 percent compared with the same time last year, while nonfatal shootings were up slightly, from 414 at that time last year to 427 this year.

Tuesday

Redbook

8:55 AM ET

8:55 AM ET

S&P Case-Shiller HPI

9:00 AM ET

9:00 AM ET

Consumer Confidence

10:00 AM ET

10:00 AM ET

State Street Investor Confidence Index

10:00 AM ET

10:00 AM ET

4-Week Bill Auction11:30 AM ET

Some thoughts, Presidential debates are coming up (I doubt that Hillary will do well, Trump and election uncertainty will be bearish for the dollar shorter term), we also have Debt Ceiling at the end of September and also the Yuan is added to the IMF-basket on 2nd October.

Not a chance in hell the Fed is going to raise interest rates in September to risk a financial and economic fall out, Yellen is in the pocket of the Democratic Party.

If some unemployment numbers are not so well, then the Dollar will decline sharply, which could be bullish for US equities.

Some thoughts, Presidential debates are coming up (I doubt that Hillary will do well, Trump and election uncertainty will be bearish for the dollar shorter term), we also have Debt Ceiling at the end of September and also the Yuan is added to the IMF-basket on 2nd October.

Not a chance in hell the Fed is going to raise interest rates in September to risk a financial and economic fall out, Yellen is in the pocket of the Democratic Party.

If some unemployment numbers are not so well, then the Dollar will decline sharply, which could be bullish for US equities.

Monday, August 29, 2016

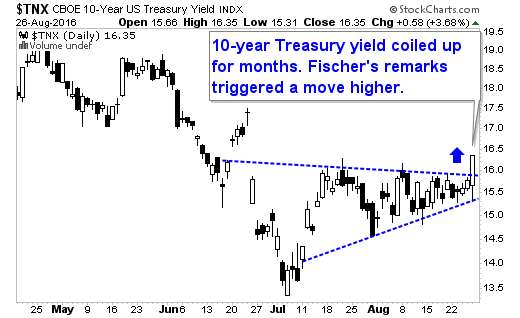

T'NX

By the way, Fischer has a history of being full of baloney. The market doesn't remember, but last August he hinted strongly at a September rate hike and it never happened.

Where various Fed governors stand on rate hikes: LINK

Brad DeLong on what Fischer should have said. LINK

SC high school bans American flags at football game

http://wncn.com/2016/08/29/sc-high-school-bans-american-flags-at-football-game/

The principal of Travelers Rest High School released a statement Saturday afternoon after complaints on social media after a students were not allowed to bring American flags to a football game Friday night.

Saturday evening Greenville County Schools released a statement saying the district “encourages and supports the appropriate display of the United States Flag in accord with the United States Flag Code.”

The statement went on to say that the district, “[does] not condone the use of the Flag to shield unsportsmanlike or inappropriate conduct.”

Read the full statement below.

The principal of Travelers Rest High School released a statement Saturday afternoon after complaints on social media after a students were not allowed to bring American flags to a football game Friday night.

Saturday evening Greenville County Schools released a statement saying the district “encourages and supports the appropriate display of the United States Flag in accord with the United States Flag Code.”

The statement went on to say that the district, “[does] not condone the use of the Flag to shield unsportsmanlike or inappropriate conduct.”

Read the full statement below.

Trump To Launch Major Attack Ad Campaign Against Hillary; "She is a jobs killer"

http://hosted.ap.org/dynamic/stories/U/US_CAMPAIGN_2016_TRUMP_ADS?SITE=AP&SECTION=HOME&TEMPLATE=DEFAULT&CTIME=2016-08-29-11-06-51

Donald Trump's

campaign is making its biggest general election ad buy to date, with

plans to spend upward of $10 million on commercials airing over the next

week or so.

The campaign is expecting to air a

new ad, which paints rival Hillary Clinton as a job-killer, as soon as

Monday in nine states: Ohio, Pennsylvania, North Carolina and Florida,

where the campaign has already been on the air, along with New

Hampshire, Virginia, Iowa, Colorado and Nevada - all battleground

states.

German Savers Lose Faith in Banks, Stash Cash at Home

http://www.wsj.com/articles/german-savers-lose-faith-in-banks-stash-cash-at-home-1472485225

For years, Germans kept socking money away in savings accounts despite plunging interest rates. Savers deemed the accounts secure, and they still offered easy cash access. But recently, many have lost faith.

“It doesn’t pay to keep money in the bank, and on top of that you’re being taxed on it,” said Uwe Wiese, an 82-year-old pensioner who recently bought a home safe to stash roughly €53,000 ($59,344), including part of his company pension that he took as a payout.

Interest rates’ plunge into negative territory is now accelerating demand for impregnable metal boxes.

Burg-Waechter KG, Germany’s biggest safe manufacturer, posted a 25% jump in sales of home safes in the first half of this year compared with the year earlier, said sales chief Dietmar Schake, citing “significantly higher demand for safes by private individuals, mainly in Germany.”

For years, Germans kept socking money away in savings accounts despite plunging interest rates. Savers deemed the accounts secure, and they still offered easy cash access. But recently, many have lost faith.

“It doesn’t pay to keep money in the bank, and on top of that you’re being taxed on it,” said Uwe Wiese, an 82-year-old pensioner who recently bought a home safe to stash roughly €53,000 ($59,344), including part of his company pension that he took as a payout.

Interest rates’ plunge into negative territory is now accelerating demand for impregnable metal boxes.

Burg-Waechter KG, Germany’s biggest safe manufacturer, posted a 25% jump in sales of home safes in the first half of this year compared with the year earlier, said sales chief Dietmar Schake, citing “significantly higher demand for safes by private individuals, mainly in Germany.”

Nearly 10000 workers sue Chipotle for unpaid wages

http://money.cnn.com/2016/08/29/news/economy/chipotle-lawsuit-nearly-10000-workers/index.html

Current and former Chipotle (CMG) employees claim that the company made them work extra hours "off the clock" without paying them. It's a practice known as wage theft, and Chipotle is allegedly doing it all over the United States.

"Chipotle routinely requires hourly-paid restaurant

employees to punch out, and then continue working until they are given

permission to leave," according to the class action lawsuit known as

Turner v. Chipotle. It's named after a former Chipotle manager in

Colorado, Leah Turner, who claims she had to work without pay and was

told to make workers under her do the same in order to meet budget goals.

Current and former Chipotle (CMG) employees claim that the company made them work extra hours "off the clock" without paying them. It's a practice known as wage theft, and Chipotle is allegedly doing it all over the United States.

Slush funds to pay 'personal consultant' Huma Abedin, a $34,000 a night Caribbean holiday for daughter Chelsea and payoffs to silence Bill's sex accusers - How Hillary has used donations to the Clinton Foundation as her ‘personal piggy bank’

http://www.dailymail.co.uk/news/article-3659123/Slush-funds-pay-personal-consultant-Huma-Abedin-luxe-Caribbean-holiday-daughter-Chelsea-payoffs-silence-Bill-s-sex-accusers-Hillary-used-donations-Clinton-Foundation-personal-piggy-bank.html#ixzz4Ik4QSxJZ

The Clinton

Foundation is 'a vast, criminal conspiracy' and 'a slush fund for

grifters' with thousands of honest people who are victims after

contributing their hard-earned money to what they believed would be used

for philanthropic causes.

In

truth, the money that was donated to help earthquake victims in India

and Haiti and HIV/AIDs sufferers in the Third World has mostly enriched

the Clintons and their friends through scams spanning the globe, claims

author Jerome Corsi in his book, Partners in Crime: The Clintons' Scheme to Monetize the White House for Personal Profit, which will be published in August.

Driven

by insatiable greed while crying they were near-broke, the couple

schemed and Hillary used her position as secretary of state to leverage

lucrative deals for the Foundation as well as six-figure speaking fees

for Bill Clinton.

The

scheme engineered through the Foundation has enriched the Clintons by

hundreds of millions of dollars as well as adding $2billion to the

Clinton Foundation and raising $1billion for Hillary's second run for

the presidency, writes Corsi in his upcoming book.

Silver bull run just getting started: Tradebulls

http://www.financialexpress.com/markets/commodities/silver-bull-run-just-getting-started-tradebulls/357061/

It has been a good year for precious metals, particularly for gold and silver. If we look at gold, it has performed 28 per cent while silver has outshined gold and gained by nearly 40 per cent year to date. Investors have flocked to the metal in recent months, with hedge funds expanding their bullish bets on silver to an all-time high in May, as reported by Bloomberg. Silver demand appears to be increasing and supply appears to be decreasing. Another reason for gain in silver prices is continued low-rate stimulus by the Federal Reserve, European Central Bank (ECB) and Bank of Japan. Negative rates by ECB and Bank of Japan have supported expectation for continued monetary easing which is positive for bullion

It has been a good year for precious metals, particularly for gold and silver. If we look at gold, it has performed 28 per cent while silver has outshined gold and gained by nearly 40 per cent year to date. Investors have flocked to the metal in recent months, with hedge funds expanding their bullish bets on silver to an all-time high in May, as reported by Bloomberg. Silver demand appears to be increasing and supply appears to be decreasing. Another reason for gain in silver prices is continued low-rate stimulus by the Federal Reserve, European Central Bank (ECB) and Bank of Japan. Negative rates by ECB and Bank of Japan have supported expectation for continued monetary easing which is positive for bullion

Dallas Fed Manufacturing index lower in August at -6.2 vs -1.3 last month

Lower than expectations at -3.9

Earlier today, the Dallas

Fed Manufacturing index fell in the current month. This is report on the

state of the economy in the state of Texas. Texas has been a large

contributor to the economy in the US. Of course the state is large in

size and also large in energy, and cattle/farming and also in technology

(Dell is headquartered in the state) and other corporate businesses.

The

index fell to -6.2 in August vs. exepctations of -3.9 and -1.3 last

month. Below is a look at the details of the report. Although lower,

the numbers for the current month are mostly higher than the 6-month

averages. Which is a more positive trend.

Norwegian Central Bank Discloses Nearly $1 Billion in US Gold and Silver...

There's an awful lot of gold being accumulated by central banks.

Here are the gold and silver mining shares disclosed by Norges Bank and their values* as of June 30, 2015.

IMF’s ‘Substitution Fund’ to kick-start SDR as new global currency?

http://www.cdfund.com/wp-content/uploads/2016/08/SDR-Special-aug2016-DEF.pdf

After seven years of Chinese pressure, a plan allowing investors to exchange their U.S.

Treasury holdings for SDRs through a ‘substitution fund’ is being discussed

The Big Reset (2013) fully explains the need for a major reform of the world’s financial system.

At that time of publication, most people still had no clue what form the unfolding financial

endgame would take. A few years further on, and as interest rates have reached a level not seen

in 500 years, many are now starting to agree major monetary changes are needed urgently.

After seven years of Chinese pressure, a plan allowing investors to exchange their U.S.

Treasury holdings for SDRs through a ‘substitution fund’ is being discussed

The Big Reset (2013) fully explains the need for a major reform of the world’s financial system.

At that time of publication, most people still had no clue what form the unfolding financial

endgame would take. A few years further on, and as interest rates have reached a level not seen

in 500 years, many are now starting to agree major monetary changes are needed urgently.

Sunday, August 28, 2016

The warning

The founders specifically warned that Congress, backed by a standing

army, might one day move to disarm the American people, leaving citizens

toothless to oppose tyranny.

Are we witnessing the start of something the founders warned of?

Retired Army Gen. Peter Chiarelli is now among those campaigning for deeper layers of civilian gun control. At Time, Chiarelli writes he's now part of something called the Veterans Coalition for Common Sense:

Pretty damn bold. Chiarelli wraps himself in the Constitution while advocating infringement of both the Second Amendment and citizen rights to due process. The Constitution considers an accused person innocent until proven guilty. Chiarelli and his cohorts wish to begin infringing on citizens rights based on mere suspicions, some of which may not even risk to the level of triggering active law enforcement investigation.

The founders warned of guys like Chiarelli and his would-be rights-crushing cohorts.

Ever read Liberty or Empire by Patrick Henry? By some accounts, it's Henry's second most famous speech, saying in part:

We're now seeing an orchestrated move by political elites to un-do the constitutional safeguards the founders put in place, and that those who push for the un-doing count on dumbed-down Americans who fail to see what's falsely touted as common sense by today's political class and their allies would have been labeled by the founders as steps toward tyranny.

Are we witnessing the start of something the founders warned of?

Retired Army Gen. Peter Chiarelli is now among those campaigning for deeper layers of civilian gun control. At Time, Chiarelli writes he's now part of something called the Veterans Coalition for Common Sense:

Some of us are combat veterans. Some of us are gun owners. All of us were trained in the responsible use of firearms and to have respect for their incredible power. All of us swore an oath to defend our Constitution and to defend the homeland. And we all agree on this: our country is in the grips of a gun-violence crisis...The term common sense must resonate well with average folk and focus groups. That's probably why so many politicians use the term to accompany twisted words and bamboozling proposals that put our rights at risk.

The policies we support—closing the loopholes in our background check system and prohibiting known and suspected terrorists from legally buying guns—are not controversial. In fact, we are not asking our leaders to do anything that is not supported by the overwhelming majority of Americans, including gun owners. We are simply asking them to use common sense to save lives.

Pretty damn bold. Chiarelli wraps himself in the Constitution while advocating infringement of both the Second Amendment and citizen rights to due process. The Constitution considers an accused person innocent until proven guilty. Chiarelli and his cohorts wish to begin infringing on citizens rights based on mere suspicions, some of which may not even risk to the level of triggering active law enforcement investigation.

The founders warned of guys like Chiarelli and his would-be rights-crushing cohorts.

Ever read Liberty or Empire by Patrick Henry? By some accounts, it's Henry's second most famous speech, saying in part:

The honorable gentleman who presides told us that, to prevent abuses in our government, we will assemble in convention, recall our delegated powers, and punish our servants for abusing the trust reposed in them. Oh, sir! we should have fine times, indeed, if, to punish tyrants, it were only sufficient to assemble the people! Your arms, wherewith you could defend yourselves, are gone; and you have no longer an aristocratical, no longer a democratical spirit. Did you ever read of any revolution in a nation, brought about by the punishment of those in power, inflicted by those who had no power at all? You read of a riot act in a country which is called one of the freest in the world, where a few neighbors can not assemble without the risk of being shot by a hired soldiery, the engines of despotism. We may see such an act in America.Henry's speech was delivered in 1788 to the Virginia legislature testifying to his insistence that a Bill of Rights be included with ratification of the Constitution.

We're now seeing an orchestrated move by political elites to un-do the constitutional safeguards the founders put in place, and that those who push for the un-doing count on dumbed-down Americans who fail to see what's falsely touted as common sense by today's political class and their allies would have been labeled by the founders as steps toward tyranny.

Has the US Quietly Emptied the Denver Mint of Over 1,300 Tonnes of Gold?

https://www.bullionstar.com/blogs/ronan-manly/gold-bullion-stored-us-mint-denver/

[The Mint's Web site stated] "Today, the United States Mint at Denver manufactures all denominations of circulating coins, coin dies, the Denver "D" portion of the annual uncirculated coin sets and commemorative coins authorized by the U. S. Congress. It also stores gold and silver bullion."''... Less than a month later, on September 8, 2014, the above paragraph had been subtly changed to the following, and the words `gold and' had been removed...''

[The Mint's Web site stated] "Today, the United States Mint at Denver manufactures all denominations of circulating coins, coin dies, the Denver "D" portion of the annual uncirculated coin sets and commemorative coins authorized by the U. S. Congress. It also stores gold and silver bullion."''... Less than a month later, on September 8, 2014, the above paragraph had been subtly changed to the following, and the words `gold and' had been removed...''

Friday, August 26, 2016

Who's Pulling The Strings?

http://market-ticker.org/akcs-www?post=231481

It must be nice to have the ability to take otherwise taxable income and give it to your family friends while at the same time paying no taxes on it!

Now isn't that special?

All the screaming about Trump's tax return is a distraction which the media is more than willing to go along with by not focusing on the fact that Clinton really didn't give anything to charity at all; she and Bill instead abused the tax code to funnel "earnings" tax free to their family friends!

It must be nice to have the ability to take otherwise taxable income and give it to your family friends while at the same time paying no taxes on it!

Now isn't that special?

All the screaming about Trump's tax return is a distraction which the media is more than willing to go along with by not focusing on the fact that Clinton really didn't give anything to charity at all; she and Bill instead abused the tax code to funnel "earnings" tax free to their family friends!

Portugal Gets EU Approval to Inject $5 bln Into Ailing Bank

http://www.cnbc.com/2016/08/25/portugal-minister-on-bank-recap-plan-this-is-another-big-step-for-our-financial-system.html

The plan was agreed late on Tuesday afternoon. It would see Portugal pump up to 2.7 billion euros of state funds into Caixa, transfer 500 million euros of its ParCaixa shares to Caixa and convert 960 million euros of contingent convertible bonds into equity.

...

Meanwhile, Caixa will issue highly subordinated debt worth around 1.0 billion euros that will be compliant with regulatory capital ratios designed to bolster banks' ability to withstand financial shocks.

This follows negotiations with Brussels officials, aimed at ensuring the plan is not viewed as state-aid to the bank, which would add to Portugal's problematically high budget deficit.

Although the government would put money into the bank, the hope is that the returns for the state would outweigh the cash injection.

Uh-huh. Since now we're obviously about to go into an economic boom period, we're sure the Portuguese government will make money on this definitely-not-a-bailout cash injection...

The plan was agreed late on Tuesday afternoon. It would see Portugal pump up to 2.7 billion euros of state funds into Caixa, transfer 500 million euros of its ParCaixa shares to Caixa and convert 960 million euros of contingent convertible bonds into equity.

...

Meanwhile, Caixa will issue highly subordinated debt worth around 1.0 billion euros that will be compliant with regulatory capital ratios designed to bolster banks' ability to withstand financial shocks.

This follows negotiations with Brussels officials, aimed at ensuring the plan is not viewed as state-aid to the bank, which would add to Portugal's problematically high budget deficit.

Although the government would put money into the bank, the hope is that the returns for the state would outweigh the cash injection.

Uh-huh. Since now we're obviously about to go into an economic boom period, we're sure the Portuguese government will make money on this definitely-not-a-bailout cash injection...

Broken Chessboard: Brzezinski Gives Up on Empire

http://www.counterpunch.org/2016/08/25/the-broken-chessboard-brzezinski-gives-up-on-empire/

The main architect of Washington's plan to rule the world has abandoned the scheme and called for the forging of ties with Russia and China. While Zbigniew Brzezinski's article in The American Interest titled "Towards a Global Realignment" has largely been ignored by the media, it shows that powerful members of the policymaking establishment no longer believe that Washington will prevail in its quest to extent US hegemony across the Middle East and Asia. Brzezinski, who was the main proponent of this idea and who drew up the blueprint for imperial expansion in his 1997 book The Grand Chessboard: American Primacy and Its Geostrategic Imperatives, has done an about-face and called for a dramatic revising of the strategy.

...

Naturally, in a short 1,500-word article, Brzezniski can't cover all the challenges (or threats) the US might face in the future. But it's clear that what he's most worried about is the strengthening of economic, political and military ties between Russia, China, Iran, Turkey and the other Central Asian states.

The main architect of Washington's plan to rule the world has abandoned the scheme and called for the forging of ties with Russia and China. While Zbigniew Brzezinski's article in The American Interest titled "Towards a Global Realignment" has largely been ignored by the media, it shows that powerful members of the policymaking establishment no longer believe that Washington will prevail in its quest to extent US hegemony across the Middle East and Asia. Brzezinski, who was the main proponent of this idea and who drew up the blueprint for imperial expansion in his 1997 book The Grand Chessboard: American Primacy and Its Geostrategic Imperatives, has done an about-face and called for a dramatic revising of the strategy.

...

Naturally, in a short 1,500-word article, Brzezniski can't cover all the challenges (or threats) the US might face in the future. But it's clear that what he's most worried about is the strengthening of economic, political and military ties between Russia, China, Iran, Turkey and the other Central Asian states.

Blue State Blues: Fact-Check — Top 20 Lies in Hillary’s ‘Alt-Right’ Speech

http://www.breitbart.com/big-government/2016/08/26/blue-state-blues-fact-check-top-20-lies-hillarys-alt-right-speech/

Andrew added: “They need to marginalize and demonize those that would stand up to their hardball, toxic, and antidemocratic tactics … But it won’t work. Given a fair hearing, given just the slightest exposure — and the American people will rise to the occasion. They see these tactics for what they are.”

Conservatives will never be “given” a fair hearing. But I made sure I was personally on hand in Reno to hear Hillary Clinton’s lies, wearing my Breitbart shirt.

Andrew added: “They need to marginalize and demonize those that would stand up to their hardball, toxic, and antidemocratic tactics … But it won’t work. Given a fair hearing, given just the slightest exposure — and the American people will rise to the occasion. They see these tactics for what they are.”

Conservatives will never be “given” a fair hearing. But I made sure I was personally on hand in Reno to hear Hillary Clinton’s lies, wearing my Breitbart shirt.

Fed's Fischer: Yellen's comments are consistent with possible Sept hike

- Suggests rate hike this year is possible

- Economic picture is very complex

- Evidence is that the economy has strengthened

- We've had very strong hiring reports recently

- Inflation has been growing

- On employment, we're doing well

- Fed is not behind the curve on hikes

- Fiscal stimulus would be good for the economy

Donald Trump full interview w/ Anderson Cooper CNN today 8/25 – “She should be in jail. You know it, the FBI Director knows it, …”. Great interview, Anderson gives him time to talk, but CNN video people deceiving with the captions again.

Captions in order below. For reference, I quickly skipped through a

Clinton interview (same length) and it had about five changes… Trump was

covering nearly his entire platform in this interview.

TRUMP SHIFTS AGAIN ON IMMIGRATION

TRUMP: “WE’RE GOING TO BUILD A GREAT WALL”

TRUMP: “BAD DUDES” HERE ILLEGALLY WILL BE “OUT”

TRUMP: POLICE KNOW WHO THE “BAD DUDES” ARE

TRUMP: WE’RE GOING TO END SANCTUARY CITIES

TRUMP ON IMMIGRATION SHIFT: “I DON’T THINK IT’S A SOFTENING”

TRUMP ON ILLEGAL IMMIGRANTS: WE KNOW THE BAD ONES

TRUMP: NO PATH TO LEGALIZATION UNLESS THEY LEAVE AND COME BACK

TRUMP: WE’RE GOING TO GO WITH THE EXISTING LAWS

TRUMP: WE’RE GOING TO HAVE A STRONG BORDER

TRUMP: WE’RE GONNA STOP ALL DRUG TRAFFIC

TRUMP: THERE’S NO LEGALIZATION, NO AMNESTY

TRUMP DIGS IN ON BIGOTRY CLAIM ABOUT CLINTON

TRUMP: CLINTON IS “SELLING” AFRICAN AMERICANS “DOWN THE TUBES”

TRUMP: CLINTON’S POLICIES ARE BIGOTED BECAUSE SHE KNOWS THEY WON’T WORK

TRUMP: CLINTON HAS BEEN EXTREMELY BAD FOR AFRICAN AMERICANS, HISPANICS

TRUMP: WE’RE GOING TO DO WELL WITH AFRICAN AMERICANS

TRUMP: I DON’T THINK AFRICAN AMERICANS ARE INSULTED BY MY LANGUAGE

TRUMP: I CAN FIX THE INNER CITIES, CLINTON CAN’T

TRUMP RESPONDS TO CLINTON’S ALT-RIGHT ATTACKS

TRUMP: WE’RE BRINGING IN LOVE, NOT HATE

TRUMP ON ALT-RIGHT: I DON’T EVEN KNOW WHAT IT IS

TRUMP: CLINTON IS ALL TALK, NO ACTION

TRUMP ON RACIAL DISCRIMINATION LAWSUIT: THEY FOUND NOTHING

TRUMP: THEY SETTLED THE CASE, WE PAID NO MONEY

TRUMP SHIFTS AGAIN ON IMMIGRATION

TRUMP: “WE’RE GOING TO BUILD A GREAT WALL”

TRUMP: “BAD DUDES” HERE ILLEGALLY WILL BE “OUT”

TRUMP: POLICE KNOW WHO THE “BAD DUDES” ARE

TRUMP: WE’RE GOING TO END SANCTUARY CITIES

TRUMP ON IMMIGRATION SHIFT: “I DON’T THINK IT’S A SOFTENING”

TRUMP ON ILLEGAL IMMIGRANTS: WE KNOW THE BAD ONES

TRUMP: NO PATH TO LEGALIZATION UNLESS THEY LEAVE AND COME BACK

TRUMP: WE’RE GOING TO GO WITH THE EXISTING LAWS

TRUMP: WE’RE GOING TO HAVE A STRONG BORDER

TRUMP: WE’RE GONNA STOP ALL DRUG TRAFFIC

TRUMP: THERE’S NO LEGALIZATION, NO AMNESTY

TRUMP DIGS IN ON BIGOTRY CLAIM ABOUT CLINTON

TRUMP: CLINTON IS “SELLING” AFRICAN AMERICANS “DOWN THE TUBES”

TRUMP: CLINTON’S POLICIES ARE BIGOTED BECAUSE SHE KNOWS THEY WON’T WORK

TRUMP: CLINTON HAS BEEN EXTREMELY BAD FOR AFRICAN AMERICANS, HISPANICS

TRUMP: WE’RE GOING TO DO WELL WITH AFRICAN AMERICANS

TRUMP: I DON’T THINK AFRICAN AMERICANS ARE INSULTED BY MY LANGUAGE

TRUMP: I CAN FIX THE INNER CITIES, CLINTON CAN’T

TRUMP RESPONDS TO CLINTON’S ALT-RIGHT ATTACKS

TRUMP: WE’RE BRINGING IN LOVE, NOT HATE

TRUMP ON ALT-RIGHT: I DON’T EVEN KNOW WHAT IT IS

TRUMP: CLINTON IS ALL TALK, NO ACTION

TRUMP ON RACIAL DISCRIMINATION LAWSUIT: THEY FOUND NOTHING

TRUMP: THEY SETTLED THE CASE, WE PAID NO MONEY

Japan July consumer prices post biggest annual fall in three yrs (TIME FOR A NIRP DOUBLE-DOWN?)

http://www.reuters.com/article/us-japan-economy-cpi-idUSKCN111004

Japan's consumer prices fell in July by the most in more than three years as more firms delayed price hikes due to weak consumption, keeping the central bank under pressure to expand an already massive stimulus program.

The gloomy data reinforces a dominant market view that premier Shinzo Abe's stimulus program have failed to dislodge the deflationary mindset prevailing among businesses and consumers.

...

"Given how prices are behaving and how the BOJ is asked to cooperate with Abe to beat deflation, it's very hard to think the BOJ will unwind stimulus any time soon," said Takeshi Minami, chief economist at Norinchukin Research Institute.

"Instead, the September analysis will probably lay the grounds for a deepening of negative interest rates."

Japan's consumer prices fell in July by the most in more than three years as more firms delayed price hikes due to weak consumption, keeping the central bank under pressure to expand an already massive stimulus program.

The gloomy data reinforces a dominant market view that premier Shinzo Abe's stimulus program have failed to dislodge the deflationary mindset prevailing among businesses and consumers.

...

"Given how prices are behaving and how the BOJ is asked to cooperate with Abe to beat deflation, it's very hard to think the BOJ will unwind stimulus any time soon," said Takeshi Minami, chief economist at Norinchukin Research Institute.

"Instead, the September analysis will probably lay the grounds for a deepening of negative interest rates."

Yemen missiles hit facilities of Saudi oil giant Aramco

http://presstv.com/Detail/2016/08/26/481761/Yemen-Saudi-Arabia-Aramco

The retaliatory attack took place on Friday, hitting targets in Saudi Arabia’s Jizan region and causing considerable damage to the Aramco facilities there, Yemen’s al-Masirah television reported.

The Saudi military has been pounding Yemen since March last year to undermine Yemen’s Houthi Ansarullah movement and to restore power to the former president, Abd Rabbuh Mansur Hadi, a staunch ally of Riyadh.

Nearly 10,000 people, most of them civilians, have been killed in Riyadh’s military aggression which lacks any international mandate.

The retaliatory attack took place on Friday, hitting targets in Saudi Arabia’s Jizan region and causing considerable damage to the Aramco facilities there, Yemen’s al-Masirah television reported.

The Saudi military has been pounding Yemen since March last year to undermine Yemen’s Houthi Ansarullah movement and to restore power to the former president, Abd Rabbuh Mansur Hadi, a staunch ally of Riyadh.

Nearly 10,000 people, most of them civilians, have been killed in Riyadh’s military aggression which lacks any international mandate.

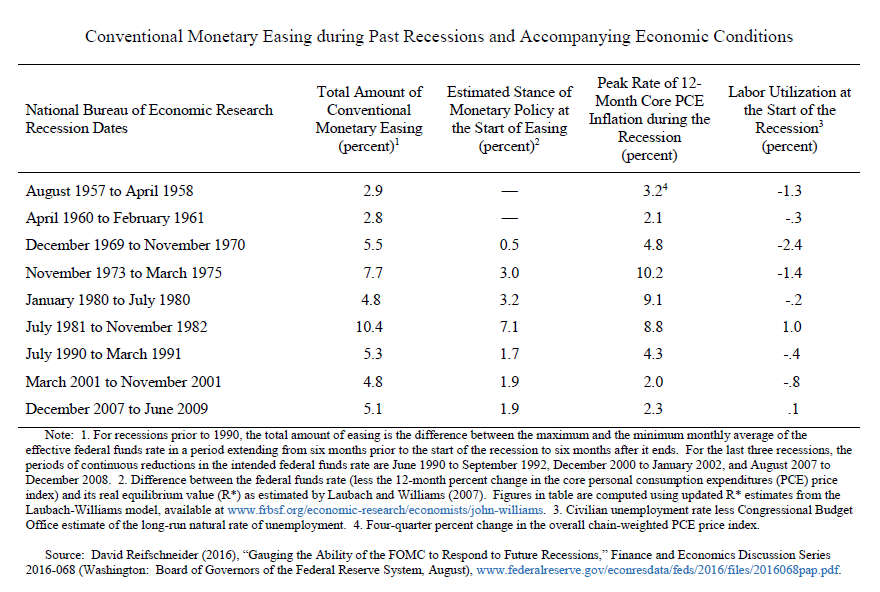

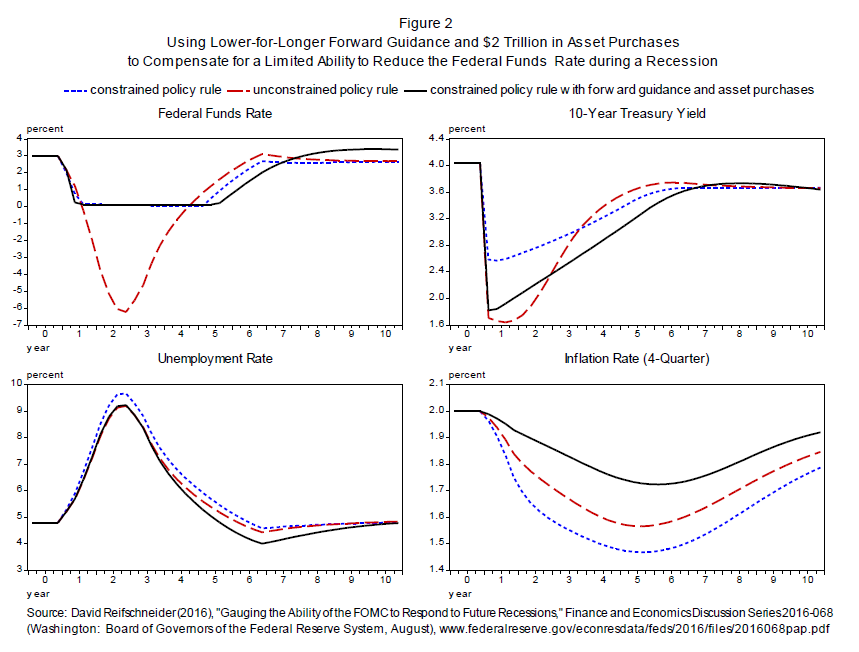

Full text of Yellen's speech at Jackson Hole August 26, 2016

The Global Financial Crisis and Great Recession posed daunting new

challenges for central banks around the world and spurred innovations in

the design, implementation, and communication of monetary policy. With

the U.S. economy now nearing the Federal Reserve's statutory goals of

maximum employment and price stability, this conference provides a

timely opportunity to consider how the lessons we learned are likely to

influence the conduct of monetary policy in the future.

The theme of the conference, "Designing Resilient Monetary Policy Frameworks for the Future," encompasses many aspects of monetary policy, from the nitty-gritty details of implementing policy in financial markets to broader questions about how policy affects the economy. Within the operational realm, key choices include the selection of policy instruments, the specific markets in which the central bank participates, and the size and structure of the central bank's balance sheet. These topics are of great importance to the Federal Reserve. As noted in the minutes of last month's Federal Open Market Committee (FOMC) meeting, we are studying many issues related to policy implementation, research which ultimately will inform the FOMC's views on how to most effectively conduct monetary policy in the years ahead. I expect that the work discussed at this conference will make valuable contributions to the understanding of many of these important issues.

My focus today will be the policy tools that are needed to ensure that we have a resilient monetary policy framework. In particular, I will focus on whether our existing tools are adequate to respond to future economic downturns. As I will argue, one lesson from the crisis is that our pre-crisis toolkit was inadequate to address the range of economic circumstances that we faced. Looking ahead, we will likely need to retain many of the monetary policy tools that were developed to promote recovery from the crisis. In addition, policymakers inside and outside the Fed may wish at some point to consider additional options to secure a strong and resilient economy. But before I turn to these longer-run issues, I would like to offer a few remarks on the near-term outlook for the U.S. economy and the potential implications for monetary policy.

Current Economic Situation and Outlook

U.S. economic activity continues to expand, led by solid growth in household spending. But business investment remains soft and subdued foreign demand and the appreciation of the dollar since mid-2014 continue to restrain exports. While economic growth has not been rapid, it has been sufficient to generate further improvement in the labor market. Smoothing through the monthly ups and downs, job gains averaged 190,000 per month over the past three months. Although the unemployment rate has remained fairly steady this year, near 5 percent, broader measures of labor utilization have improved. Inflation has continued to run below the FOMC's objective of 2 percent, reflecting in part the transitory effects of earlier declines in energy and import prices.

Looking ahead, the FOMC expects moderate growth in real gross domestic product (GDP), additional strengthening in the labor market, and inflation rising to 2 percent over the next few years. Based on this economic outlook, the FOMC continues to anticipate that gradual increases in the federal funds rate will be appropriate over time to achieve and sustain employment and inflation near our statutory objectives. Indeed, in light of the continued solid performance of the labor market and our outlook for economic activity and inflation, I believe the case for an increase in the federal funds rate has strengthened in recent months. Of course, our decisions always depend on the degree to which incoming data continues to confirm the Committee's outlook.

And, as ever, the economic outlook is uncertain, and so monetary policy is not on a preset course. Our ability to predict how the federal funds rate will evolve over time is quite limited because monetary policy will need to respond to whatever disturbances may buffet the economy. In addition, the level of short-term interest rates consistent with the dual mandate varies over time in response to shifts in underlying economic conditions that are often evident only in hindsight. For these reasons, the range of reasonably likely outcomes for the federal funds rate is quite wide--a point illustrated by figure 1 in your handout. The line in the center is the median path for the federal funds rate based on the FOMC's Summary of Economic Projections in June.1 The shaded region, which is based on the historical accuracy of private and government forecasters, shows a 70 percent probability that the federal funds rate will be between 0 and 3-1/4 percent at the end of next year and between 0 and 4-1/2 percent at the end of 2018.2 The reason for the wide range is that the economy is frequently buffeted by shocks and thus rarely evolves as predicted. When shocks occur and the economic outlook changes, monetary policy needs to adjust. What we do know, however, is that we want a policy toolkit that will allow us to respond to a wide range of possible conditions.

The Pre-Crisis Toolkit

Prior to the financial crisis, the Federal Reserve's monetary policy toolkit was simple but effective in the circumstances that then prevailed. Our main tool consisted of open market operations to manage the amount of reserve balances available to the banking sector.3 These operations, in turn, influenced the interest rate in the federal funds market, where banks experiencing reserve shortfalls could borrow from banks with excess reserves. Before the onset of the crisis, the volume of reserves was generally small--only about $45 billion or so.4 Thus, even small open market operations could have a significant effect on the federal funds rate. Changes in the federal funds rate would then be transmitted to other short-term interest rates, affecting longer-term interest rates and overall financial conditions and hence inflation and economic activity. This simple, light-touch system allowed the Federal Reserve to operate with a relatively small balance sheet--less than $1 trillion before the crisis--the size of which was largely determined by the need to supply enough U.S. currency to meet demand.5

The global financial crisis revealed two main shortcomings of this simple toolkit. The first was an inability to control the federal funds rate once reserves were no longer relatively scarce. Starting in late 2007, faced with acute financial market distress, the Federal Reserve created programs to keep credit flowing to households and businesses.6 The loans extended under those programs helped stabilize the financial system. But the additional reserves created by these programs, if left unchecked, would have pushed down the federal funds rate, driving it well below the FOMC's target. To prevent such an outcome, the Federal Reserve took several steps to offset (or sterilize) the effect of its liquidity and credit operations on reserves.7 By the fall of 2008, however, the reserve effects of our liquidity and credit programs threatened to become too large to sterilize via asset sales and other existing tools. Without sufficient sterilization capacity, the quantity of reserves increased to a point that the Federal Reserve had difficulty maintaining effective control over the federal funds rate.

Of course, by the end of 2008, stabilizing the federal funds rate at a level materially above zero was not an immediate concern because the economy clearly needed very low short-term interest rates. Faced with a steep rise in unemployment and declining inflation, the FOMC lowered its target for the federal funds rate to near zero, a reduction of roughly 5 percentage points over the previous year and a half. Nonetheless, a variety of policy benchmarks would, at least in hindsight, have called for pushing the federal funds rate well below zero during the economic downturn.8 That doing so was impossible highlights the second serious limitation of our pre-crisis policy toolkit: its inability to generate substantially more accommodation than could be provided by a near-zero federal funds rate.

Our Expanded Toolkit

To address the challenges posed by the financial crisis and the subsequent severe recession and slow recovery, the Federal Reserve significantly expanded its monetary policy toolkit. In 2006, the Congress had approved plans to allow the Fed, beginning in 2011, to pay interest on banks' reserve balances.9 In the fall of 2008, the Congress moved up the effective date of this authority to October 2008. That authority was essential. Paying interest on reserve balances enables the Fed to break the strong link between the quantity of reserves and the level of the federal funds rate and, in turn, allows the Federal Reserve to control short-term interest rates when reserves are plentiful. In particular, once economic conditions warrant a higher level for market interest rates, the Federal Reserve could raise the interest rate paid on excess reserves--the IOER rate. A higher IOER rate encourages banks to raise the interest rates they charge, putting upward pressure on market interest rates regardless of the level of reserves in the banking sector.

While adjusting the IOER rate is an effective way to move market interest rates when reserves are plentiful, federal funds have generally traded below this rate. This relative softness of the federal funds rate reflects, in part, the fact that only depository institutions can earn the IOER rate. To put a more effective floor under short-term interest rates, the Federal Reserve created supplementary tools to be used as needed. For instance, the overnight reverse repurchase agreement (ON RRP) facility is available to a variety of counterparties, including eligible money market funds, government-sponsored enterprises, broker-dealers, and depository institutions. Through it, eligible counterparties may invest funds overnight with the Federal Reserve at a rate determined by the FOMC. Similar to the payment of IOER, the ON RRP facility discourages participating institutions from lending at a rate substantially below that offered by the Fed.10

Our current toolkit proved effective last December. In an environment of superabundant reserves, the FOMC raised the effective federal funds rate--that is, the weighted average rate on federal funds transactions among participants in that market--by the desired amount, and we have since maintained the federal funds rate in its target range.

Two other major additions to the Fed's toolkit were large-scale asset purchases and increasingly explicit forward guidance.11 Both were used to provide additional monetary policy accommodation after short-term interest rates fell close to zero. Our purchases of Treasury and mortgage-related securities in the open market pushed down longer-term borrowing rates for millions of American families and businesses. Extended forward rate guidance--announcing that we intended to keep short-term interest rates lower for longer than might have otherwise been expected--also put significant downward pressure on longer-term borrowing rates, as did guidance regarding the size and scope of our asset purchases.

In light of the slowness of the economic recovery, some have questioned the effectiveness of asset purchases and extended forward rate guidance. But this criticism fails to consider the unusual headwinds the economy faced after the crisis. Those headwinds included substantial household and business deleveraging, unfavorable demand shocks from abroad, a period of contractionary fiscal policy, and unusually tight credit, especially for housing. Studies have found that our asset purchases and extended forward rate guidance put appreciable downward pressure on long-term interest rates and, as a result, helped spur growth in demand for goods and services, lower the unemployment rate, and prevent inflation from falling further below our 2 percent objective.12

Two of the Fed's most important new tools--our authority to pay interest on excess reserves and our asset purchases--interacted importantly. Without IOER authority, the Federal Reserve would have been reluctant to buy as many assets as it did because of the longer-run implications for controlling the stance of monetary policy. While we were buying assets aggressively to help bring the U.S. economy out of a severe recession, we also had to keep in mind whether and how we would be able to remove monetary policy accommodation when appropriate. That issue was particularly relevant because we fund our asset purchases through the creation of reserves, and those additional reserves would have made it ever more difficult for the pre-crisis toolkit to raise short-term interest rates when needed.

The FOMC considered removing accommodation by first reducing our asset holdings (including through asset sales) and raising the federal funds rate only after our balance sheet had contracted substantially. But we decided against this approach because our ability to predict the effects of changes in the balance sheet on the economy is less than that associated with changes in the federal funds rate. Excessive inflationary pressures could arise if assets were sold too slowly. Conversely, financial markets and the economy could potentially be destabilized if assets were sold too aggressively. Indeed, the so-called taper tantrum of 2013 illustrates the difficulty of predicting financial market reactions to announcements about the balance sheet. Given the uncertainty and potential costs associated with large-scale asset sales, the FOMC instead decided to begin removing monetary policy accommodation primarily by adjusting short-term interest rates rather than by actively managing its asset holdings.13 That strategy--raising short-term interest rates once the recovery was sufficiently advanced while maintaining a relatively large balance sheet and plentiful bank reserves--depended on our ability to pay interest on excess reserves.

Where Do We Go from Here?

What does the future hold for the Fed's toolkit? For starters, our ability to use interest on reserves is likely to play a key role for years to come. In part, this reflects the outlook for our balance sheet over the next few years. As the FOMC has noted in its recent statements, at some point after the process of raising the federal funds rate is well under way, we will cease or phase out reinvesting repayments of principal from our securities holdings. Once we stop reinvestment, it should take several years for our asset holdings--and the bank reserves used to finance them--to passively decline to a more normal level. But even after the volume of reserves falls substantially, IOER will still be important as a contingency tool, because we may need to purchase assets during future recessions to supplement conventional interest rate reductions.14 Forecasts now show the federal funds rate settling at about 3 percent in the longer run.15 In contrast, the federal funds rate averaged more than 7 percent between 1965 and 2000. Thus, we expect to have less scope for interest rate cuts than we have had historically.